Key highlights:

- Bitcoin slipped below $60,000 on June 26 as forced selling from futures liquidations accelerated the move.

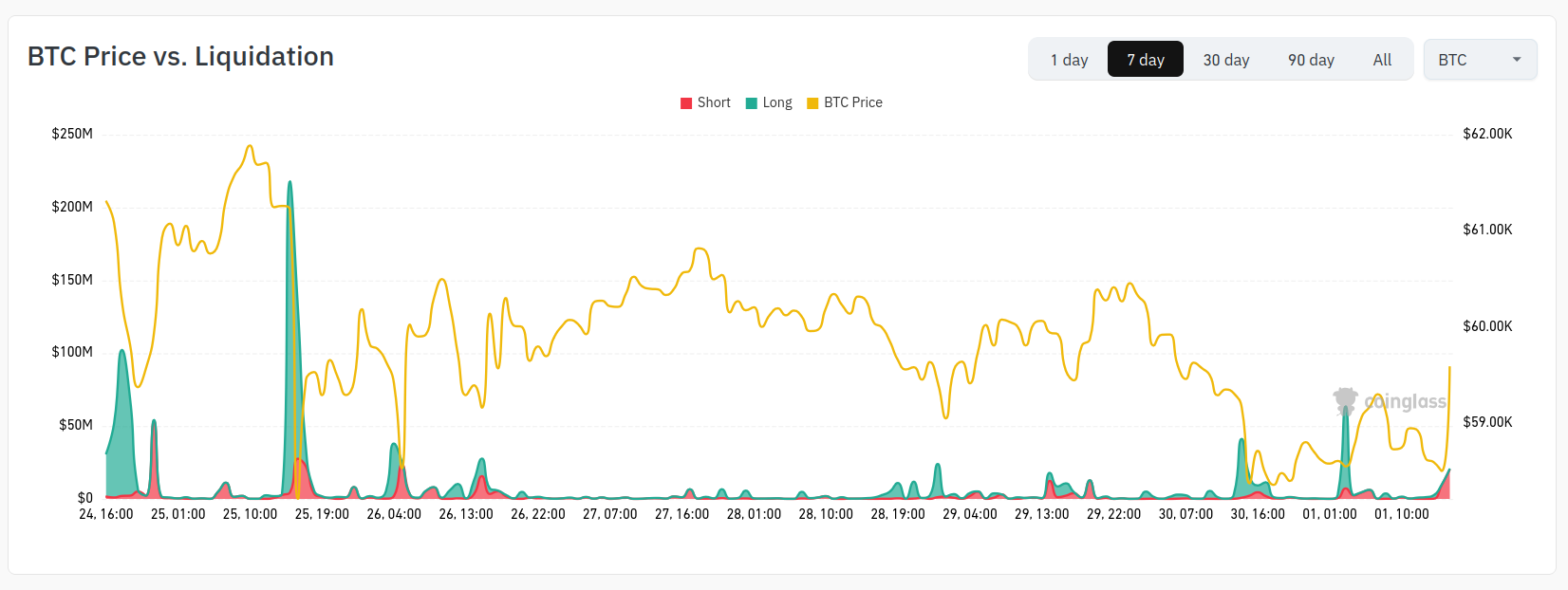

- According to CoinGlass data, there were $253 million in long Bitcoin liquidations over 24 hours, with longs accounting for 92% of all BTC liquidations

- Leverage.Trading analyst Anton Palovaara said the sell-off was amplified by exchange risk engines closing leveraged long positions through market orders

Bitcoin’s drop below $60,000 on June 26 was not driven solely by traders choosing to sell into weakness. A major part of the move came from futures liquidations, where exchanges automatically closed leveraged long positions after traders ran out of margin.

CoinGlass data reveals Bitcoin saw $253 million in long liquidations over a 24-hour period. Long positions accounted for 92% of all Bitcoin liquidations, while roughly $92 million was liquidated in a single hour as the decline accelerated.

That distinction matters. In a liquidation-heavy sell-off, the biggest source of selling pressure is often not discretionary selling from traders, but forced selling by exchanges.

The sharp decline in the Bitcoin price triggered a surge in liquidations of long positions. Source: CoinGlass

Forced liquidations amplified Bitcoin’s move lower

When a trader opens a leveraged long position, they are effectively betting that the price will rise while borrowing additional exposure from the exchange. If the market moves against them and their margin falls below the required threshold, the exchange closes the position automatically to prevent further losses.

That forced close is not a passive exit. It typically enters the market as a sell order. When many leveraged longs are liquidated at once, those forced sell orders can push the price lower, triggering additional liquidations from other traders whose positions are also near their liquidation levels.

This creates what is known as a liquidation cascade. The first wave of liquidations pushes the market down, which triggers the next wave, and that wave can trigger another. In these conditions, selling pressure can become self-reinforcing even if the original number of willing sellers was relatively limited.

The exchange became the seller

Leverage.Trading analyst Anton Palovaara said traders often focus too much on what started a sell-off, rather than what allowed it to accelerate.

According to Palovaara, almost any market event can trigger the first wave of liquidations on a leveraged derivatives platform. The severity of the cascade depends on how much leveraged positioning has built up, how closely liquidation levels are clustered, and how much liquidity is available in the order book.

“During the steepest part of a move like June 26, the biggest seller in Bitcoin is not a person. It is the exchange,” Palovaara said and continued:

“When 92 percent of what gets liquidated is longs, that is not traders selling, it is the risk engine closing them out because they ran out of margin. And every one of those closes is a market order.”

He added that this process can make the move appear like a broad market dump, even though many traders being liquidated were still trying to hold their positions.

“It sells, the price drops, the next account gets closed, and that one sells too. The trader thinks the crowd is dumping. The crowd is not dumping. The exchange is selling for them, $253 million of it, $92 million in a single hour.”

Mark price can trigger liquidations before traders expect it

One detail that is often missed is that exchanges generally use mark price, rather than the last traded price, to determine liquidations.

The mark price is designed to reduce manipulation and reflect a fairer market value, often based on index prices and funding conditions. However, this also means a trader can be liquidated even if the visible chart price appears to remain above their expected liquidation level.

For leveraged traders, this can make liquidation events feel sudden. A position may appear safe based on the last traded price, but if the mark price crosses the liquidation threshold, the exchange can still force the position closed.

June 26 followed a familiar liquidation pattern

The June 26 move was not an isolated example of forced selling amplifying Bitcoin volatility.

There was a similar pattern during the June 4 – 6 sell-off, when roughly $3 billion in leveraged crypto positions were liquidated over two days. The June 26 liquidation event was smaller in size, but the mechanism was similar: clustered leveraged positions were forced out, and those liquidations added sell pressure into an already falling market.

This is why liquidation data can be important during sharp Bitcoin moves. A large imbalance in liquidations, especially when longs dominate the total, suggests that the market is not only reacting to spot selling or changing sentiment. It may also be absorbing forced order flow from derivatives platforms.

The bottom line

Bitcoin’s fall below $60,000 on June 26 showed how leverage can turn a price decline into a cascade. The initial move lower may have had a separate trigger, but the speed and severity of the drop were amplified by forced futures liquidations.

With $253 million in long liquidations over 24 hours and $92 million liquidated in a single hour, the steepest part of the move was less about traders choosing to exit and more about exchange risk engines closing positions automatically.

For traders, the lesson is that liquidation levels can become market structure. When too much leverage builds up on one side of the market, a relatively small price move can trigger forced selling that makes the decline much larger than the original catalyst would suggest.

Source:: The Biggest Seller During Bitcoin's Drop Under $60K Wasn't the Crowd, but the Liquidation Engine