What happens when a sports‑betting affiliate suddenly starts buying Ethereum by the truckload? That’s probably not something you’ve wondered often (or ever). Still, SharpLink Gaming (SBET) found out.

For years, the Minneapolis‑based firm earned fees by sending bettors to regulated sportsbooks. That was its entire business model.

Then, in late May 2025, everything changed. SharpLink announced a $425 million private placement led by ConsenSys. The cash wasn’t earmarked for more marketing. It was for buying Ether.

SharpLink promised to make ETH its primary treasury reserve asset. Joseph Lubin, the co‑founder of Ethereum, agreed to become the company’s chairman.

The logic behind the pivot is simple: Ethereum isn’t merely a token. It’s a programmable platform for finance. By holding and staking ETH, SharpLink can earn rewards and participate directly in the network. Lubin summed it up when he said programmable assets like ETH are changing how value and trust are structured.

I’ll explore how this shift happened, what it means for SBET shareholders, and why the company believes Ethereum’s growth could turn SBET stock into a proxy for the second‑largest cryptocurrency.

Key highlights:

- SharpLink made a bold pivot from a sports-betting affiliate business to an Ethereum treasury company in 2025.

- The company raised $425 million in a private placement led by ConsenSys to buy and stake ETH as a primary treasury asset.

- SBET stock now trades as a leveraged Ethereum play, with price moves tied closely to the value and yield of ETH holdings.

- SharpLink reports weekly ETH metrics, including tokens held, ETH per share, and staking rewards, to attract transparency-focused investors.

- Joe Lubin, Ethereum co-founder, now chairs the board, which shows serious long-term belief in programmable assets like ETH.

- SBET stock carries risks, including heavy share dilution, price volatility, and changing regulation

From private placement to ETH giant

So how do you go from zero Ethereum to more coins than the Ethereum Foundation in just a few weeks? It starts with a bold fundraising move.

On May 27, 2025, SharpLink unveiled a $425 million private placement led by ConsenSys, alongside a who’s‑who of crypto venture funds. The deal involved selling roughly 69.1 million shares at $6.15 each ($6.72 for management).

Joseph Lubin signed on to become chairman of SharpLink’s board.

Just one week later, the company closed the deal. It raised the full $425 million in a mix of cash and Ether and announced that Ether would be its primary treasury reserve asset.

The press release even stated that SharpLink would use the funds to “adopt ETH…as its primary treasury reserve asset” and would continue its core marketing business alongside the crypto strategy.

From there, SharpLink wasted no time. It signed asset‑management agreements with ParaFi and Galaxy Asset Management, so that professionals would oversee its ETH treasury.

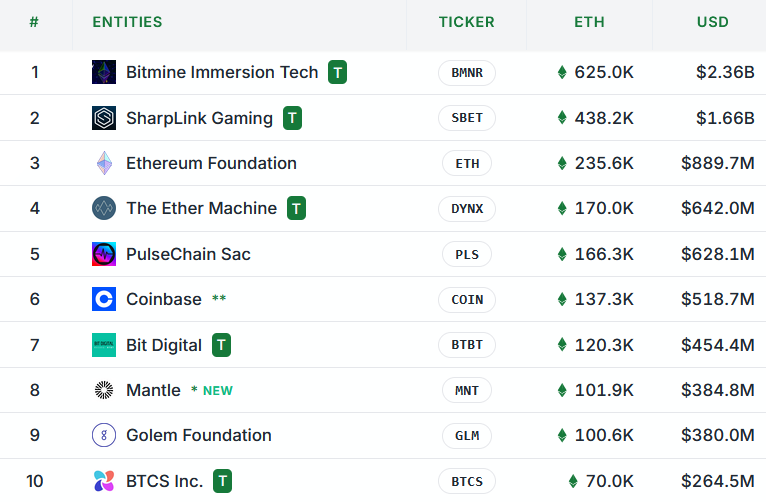

By mid‑June the company had already begun buying ETH and even held more Ether than the nonprofit Ethereum Foundation. That staggering statistic hints at the scale of SharpLink’s ambition: to build the largest corporate Ether stash in the world. And in the process, they want to offer investors a publicly traded proxy for the network.

The 10 largest Ethereum treasuries as of July 30, 2025. Image source: Strategic ETH Reserve

Building the SharpLink Ethereum treasury: weekly updates and new metrics

If the private placement was the starting pistol, SharpLink’s weekly updates have been a marathon sprint. Let’s chart the journey:

- June 24, 2025: SharpLink’s Ethereum treasury reached 188,478 ETH. In just a few days it added 12,207 ETH at an average price of $2,513 per coin. They spent about $30.7 million. To fund this, it raised $27.7 million by selling 2.5 million shares via its at‑the‑market (ATM) facility and staked 100 % of its ETH (already earning 120 ETH in rewards).

- July 20, 2025: The update got even more dramatic. SharpLink’s holdings jumped to 360,807 ETH, up 29 % from the previous week. It bought 79,949 ETH at $3,238 per coin and reported 567 ETH in cumulative staking rewards. They introduced a new metric called ETH concentration (the number of ETH per 1,000 diluted shares) and reported that it had risen to 3.06. Every 1,000 shares now represented just over 3 ETH.

- July 27, 2025: The latest update blew past previous records. SharpLink bought 77,209 ETH that week and raised $279.2 million through ATM sales. Its total holdings reached 438,200 ETH, making Sharplink’s Ethereum treasury the 2nd biggest, behind only BitMine. Cumulative staking rewards climbed to 722 ETH. ETH concentration rose to 3.40, a 70 % increase since the strategy’s launch.

Those numbers are absolutely huge. SharpLink isn’t hoarding Ether and leaving it in cold storage. It’s staking nearly all of its coins to earn yield. And it has created a per‑share metric so investors can track how much ETH backs each share.

Each weekly update reads like a scoreboard:

- Coins purchased

- Funds raised

- Concentration per share

This transparency invites investors to follow along as if they’re watching a game. Each week brings new stats.

This fast accumulation has come with continuous dilution. SharpLink keeps issuing shares to fund its purchases. Yet, because of the ETH concentration metric, investors can see whether their per‑share exposure to ETH is rising or falling.

As of July 27, the metric suggests each thousand shares represents 3.40 ETH. It’s up from 2.29 ETH just three weeks earlier.

For a company with no history of asset management, this level of disclosure is unusual and, arguably, necessary.

Why Ethereum?

If you’ve followed crypto for any length of time, you might ask: why stake your company’s future on Ethereum and not Bitcoin?

Joe Lubin has an answer. Speaking on Bloomberg on July 28, the Ethereum co‑founder said that institutions are finally recognizing Ethereum’s programmable capabilities.

- He compared ETH to digital infrastructure: a layer that lets you automate agreements and financial transactions. In contrast, Bitcoin is essentially digital gold. It’s valuable, but it doesn’t generate yield on its own.

- Lubin also noted that Ethereum treasuries can “do a lot more” with their holdings. Because ETH can be staked or used in decentralized finance, it produces a stream of rewards. SharpLink’s strategy leans heavily on this yield. By staking nearly all of its tokens, the company turns its treasury into a yield‑bearing asset rather than a speculative pile.

- Regulation clarity matters too. The Genius Act, signed into U.S. law in July 2025, created a clear framework for digital assets and smart contracts. SharpLink applauded the law, saying it removes uncertainty and helps companies harness Ethereum’s security, scalability, and smart‑contract utility.

So, the choice of Ethereum isn’t arbitrary. It’s about yield, utility, and regulatory progress. In SharpLink’s view, this combination makes ETH a more productive treasury asset than Bitcoin.

If you’re someone who likes the idea of a stock tied to a yield‑generating crypto, that’s an important distinction.

SBET Stock market reaction: boom, bust and recovery

If ETH buying and staking are the offensive plays, SBET’s share price has been the scoreboard. I’ll recap the highlights (or lowlights) below.

- May 21 to May 29: Before SharpLink revealed its crypto pivot, the SBET stock languished around $3-4. When the private placement hit the wires, enthusiasm exploded. By May 29, SBET traded at $79. That’s a 2,533 % gain in eight days. Investors rushed in to buy what they saw as a publicly traded proxy for Ethereum.

- June 23: Reality set in. The company announced plans to issue a large number of shares. This triggered fears of dilution. The stock crashed to $9 and wiped out most of its gains.

- July: As SharpLink kept buying ETH and staking it, the stock staged a partial recovery. Forbes reports that SBET traded around $32 after the company became the world’s largest corporate Ethereum holder. Still, the volatility remained extreme, with daily swings in the double digits. Currently, the stock is around $19.

Why such violent moves?

I think there are three reasons:

- First, the SBET stock has a tiny float. A few million shares can change hands quickly.

- Second, investors value SBET less on traditional metrics like earnings and more on its ETH per share. When ETH prices rise, SBET often rallies. When SharpLink announces share sales or when crypto prices wobble, SBET plunges. The Forbes analysis puts it bluntly: investors are paying for a crypto proxy, not a marketing business.

- SeekingAlpha’s summary mentions another issue: dilution risk. They note that SharpLink’s pivot left it with over 70 million potentially dilutive securities against a float of about 2.3 million shares. That means future share issues could drastically dilute per‑share exposure to ETH, even if the company keeps buying more coins.

Potential benefits and risks of ETH growth

Now to the heart of the matter: if you’re considering SBET, what are the potential rewards and what could go wrong? Let’s break it down.

How ETH growth could benefit SBET

- Price appreciation: When ETH prices climb, SharpLink’s treasury gains value. Because the company’s shares function like a leveraged call on Ether, a 10 % move in ETH can translate into a much larger percentage move in the stock (both ways).

- Staking yield: SharpLink stakes nearly all its ETH, taking advantage of the fact that ETH is one of the best coins for staking. As of July 27, cumulative staking rewards were 722 ETH. These rewards effectively increase SBET’s Ethereum holdings without additional capital.

- ETH concentration growth: By buying ETH faster than it issues shares, SharpLink increases its ETH per share. ETH concentration rose from 2.29 to 3.40 in just three weeks. If that trend continues, each share will be backed by more coins over time.

- Regulatory clarity: The Genius Act provides a legal framework for staking and smart contracts. This reduces uncertainty and could make institutional investors more comfortable with crypto treasuries.

- Institutional leadership: The arrival of Joseph Chalom, who previously led BlackRock’s Ethereum initiatives, signals that SharpLink wants to professionalize its crypto operations. Chalom’s track record includes launching the iShares Ethereum Trust. Sis experience could accelerate corporate adoption of Ethereum.

What could go wrong:

- Dilution: SharpLink continuously issues shares to fund ETH purchases. The company filed to sell up to $6 billion worth of stock, up from $1 billion previously. Each new sale lowers existing shareholders’ percentage of ETH holdings unless the purchases increase ETH per share faster than dilution.

- ETH price volatility: ETH is famously volatile (like all crypto). SharpLink’s stock magnifies that volatility. A sustained ETH bear market could slash the value of SBET’s Ethereum holdings and drive the stock into the ground.

- Regulatory risk: While the Genius Act is a positive step, staking and DeFi remain uncertain in many jurisdictions. Future regulations could limit staking rewards or require new disclosures. Many institutions remain cautious.

- Competitive pressure: BitMine Immersion, Bit Digital, and other entrants are also building ETH treasuries. BitMine holds 626k ETH, more than SharpLink’s 438k ETH. More companies chasing the same strategy could erode SharpLink’s “first‑mover” advantage and saturate the market.

- Core business uncertainties: SharpLink still runs a sports‑betting affiliate business. However, investors largely ignore this operation, and there’s a risk that management attention could be spread thin.

With these factors in mind, SBET becomes a complex instrument: part crypto proxy, part capital‑raising machine, part marketing company.

For some, that complexity presents opportunity. For others, it screams caution.

The bottom line: who should consider SBET?

So, is SBET the right way to ride Ethereum’s next bull run? The answer depends on your risk tolerance.

If you’re bullish on Ethereum and comfortable with outsized volatility, SBET offers a leveraged bet on the network. The company’s aggressive buying, staking yields, and per‑share metrics give you exposure to Ether without dealing with crypto wallets.

You also get professional management, regulatory progress, and the potential for institutional participation via leaders like Joseph Lubin and Joseph Chalom.

On the other hand, the path is riddled with risks. Serious ones. Share dilution could erode your per‑share ETH exposure, and the stock’s volatility can be rough.

Institutional analysts warn that only a handful of crypto treasury companies will succeed, and Forbes calls SBET a high‑risk way to gain Ethereum exposure, unsuited to conservative investors.

Here’s how I see it: if you simply want to own ETH, buying the token directly (or an Ethereum ETF) is probably simpler and cheaper. Yes, you’re limiting profits, but also shaving off risk.

As an investor, ask yourself:

Do you want a stock that mirrors ETH’s movements, amplified by leverage and dilution?

Answering “yes” means you should consider SBET. Answering “no” means you shouldn’t.

Source:: SharpLink's Ethereum Strategy Explained: How SBET Stock Can Benefit from ETH Growth