Crypto-backed loans are no longer niche. In 2026, they’re a practical tool for people who want cash flow, trading liquidity, or tax flexibility without selling long-term holdings.

That said, “best” depends on what you’re trying to do. Some platforms win on safety. Others win on speed, asset support, or onchain control. The right pick is the one that fits your risk level, your collateral, and how hands-on you want to be.

In this guide, I’ll share the 6 best crypto lending platforms, including their pros and cons, as well as what each of them is best for.

Let’s dive in!

What are crypto lending platforms?

A crypto lending platform lets you borrow against your crypto, or lend crypto to earn yield.

The core idea is simple. You post collateral (usually more than the value you borrow), and the platform gives you a loan in fiat, stablecoins, or another crypto asset.

It’s like a pawn loan, but your collateral is Bitcoin, ETH, or stablecoins instead of a watch.

Most loans are overcollateralized. That means if you want to borrow $10,000, you might need to lock up $20,000 or more in crypto. Why? Because crypto prices can move fast. If your collateral drops too much, the platform can liquidate part or all of it to cover the loan.

There are two broad models:

- CeFi platforms hold your collateral for you and manage the loan offchain

- DeFi platforms run through smart contracts, so you borrow onchain from liquidity pools

Both have tradeoffs. CeFi is easier, DeFi gives you more control.

Selection criteria: How I picked the 6 best crypto lending platforms

A headline crypto lending rate isn’t the only factor. A low APR doesn’t mean much if the platform has weak custody, thin liquidity, or confusing liquidation rules.

So this list focuses on the things that matter in real use:

- Security and custody practices

- Track record and transparency

- Borrowing flexibility

- Asset support

- Loan-to-value limits

- Ease of use

- Whether the platform fits a clear use case

Below, I’ll outline a table with a brief overview of each platform, followed by a more detailed analysis of each of them.

The best crypto lending platforms

| Best for | Type | Snapshot | |

|---|---|---|---|

| Ledn | Bitcoin-backed safety | CeFi | Bitcoin-first, fixed-term loans |

| Aave v3 | Onchain borrowing | DeFi | Large liquidity, no KYC |

| CoinRabbit | Fast approval | CeFi | Quick loans, high LTV options |

| Nexo | Flexible portfolios | CeFi | Credit lines, many supported assets |

| Nebeus | Stablecoin efficiency and fiat rewards | CeFi | Multiple loan types, fiat rails |

| Binance Loans | Exchange convenience | CeFi | Easy for active Binance users |

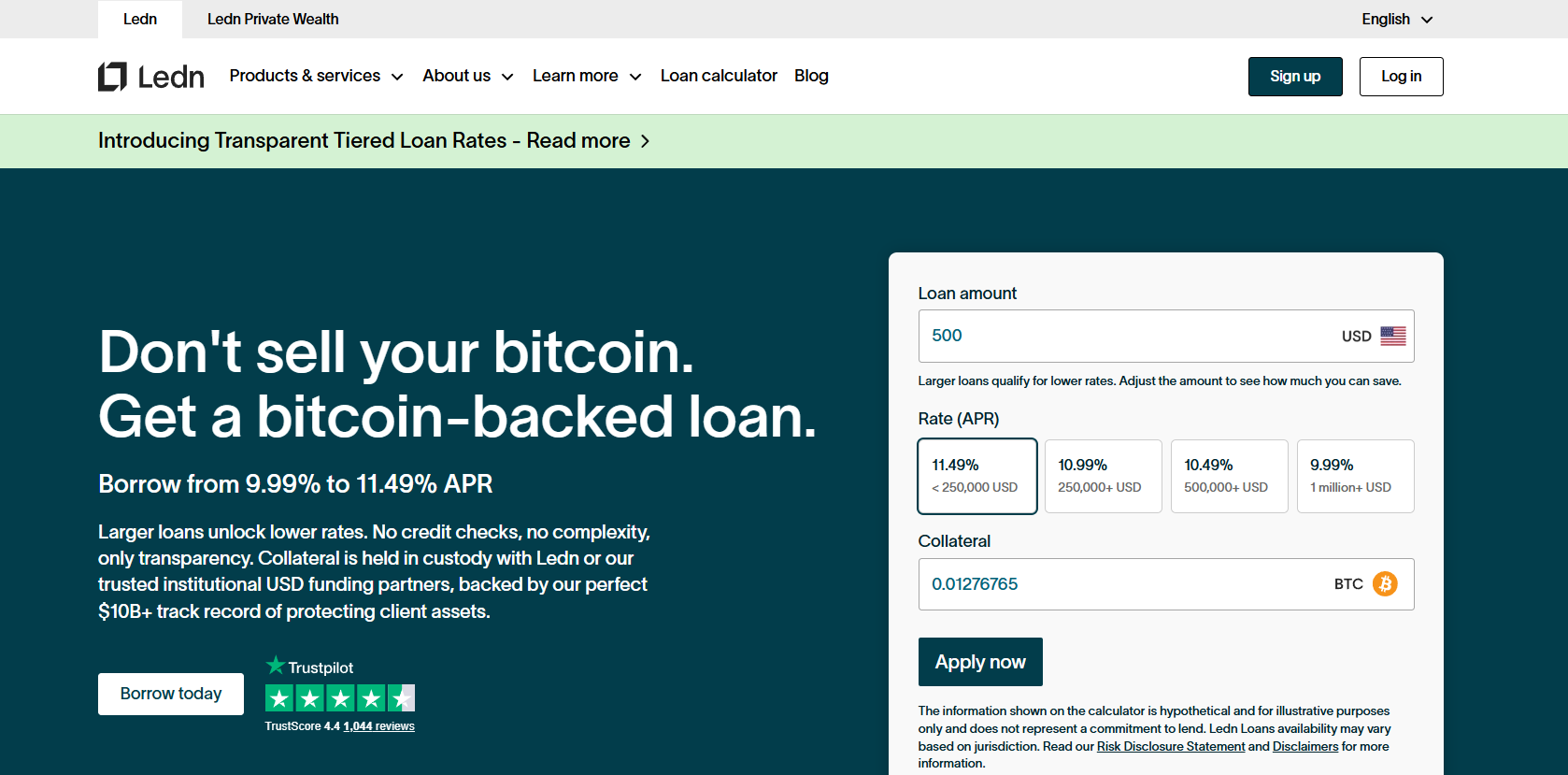

1. Ledn

Best for: the safest choice for Bitcoin-backed loans

If your main asset is Bitcoin and your main concern is trust, Ledn is the cleanest pick in this group. Its model is narrow by design, and that’s part of what makes it on the list. It focuses on Bitcoin-backed loans instead of trying to be everything at once. On top of that, Ledn is also among the best crypto savings accounts.

It offers fixed 12-month loans, no credit checks, and no monthly payments. Borrowers can repay early without penalties, and funding is often available within 24 hours after approval. Recent crypto lending rates put its APR around 9.99% to 11.49%, with better pricing on larger loans.

Ledn handles collateral differently than most platforms. The company says collateral is ring-fenced, not rehypothecated, and backed by monthly proof-of-reserves reporting. It also has a strong public track record, including more than $10 billion in loans funded and no client losses reported over eight years.

This is not the cheapest route. It’s the route for people who’d rather pay a bit more for transparency and a Bitcoin-first operating model.

Pros:

- Strong transparency and proof-of-reserves reporting

- Bitcoin-backed loans with fixed terms

- No credit checks and no monthly payments

- Excellent option for a crypto savings account

Cons:

- Limited mostly to Bitcoin collateral

- Rates aren’t the lowest on the market

- You still need to watch LTV closely in a sharp sell-off

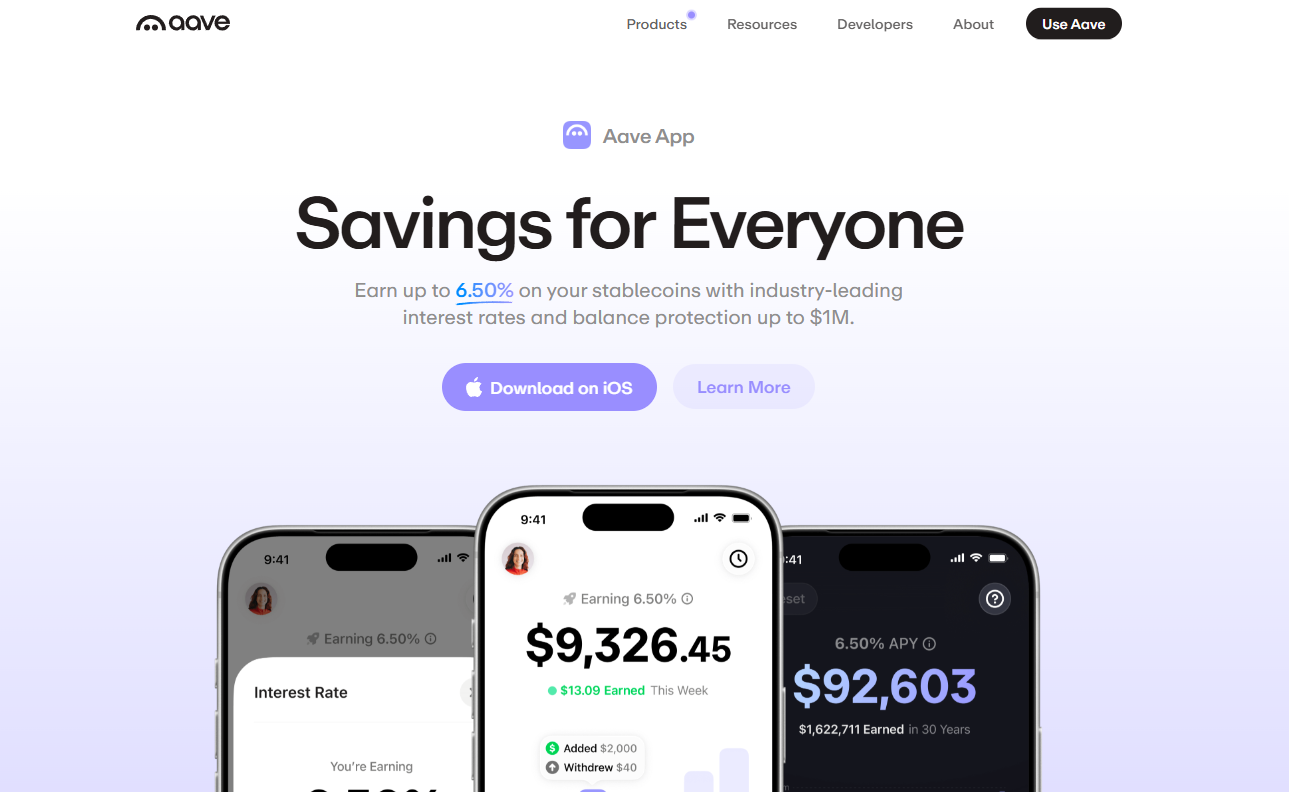

2. Aave v3

Best for: the strongest DeFi option for most users

Aave is the only DeFi lending platform on the list, and for one simple reason: it’s the best overall. If you want to borrow onchain without asking anyone’s permission, it’s hard to argue against Aave v3. It’s the biggest DeFi name in this lineup for a reason:

- Deep liquidity

- Broad market support

- Mature infrastructure

- Longevity and reputation

Aave v3 runs across multiple chains and supports major assets like ETH and stablecoins, along with other widely used tokens. Borrowing rates are variable, which means they move with supply and demand. Typical LTV levels are often in the 75% to 82% range, depending on the asset.

The big advantage is control. Aave is non-custodial, transparent onchain, and doesn’t require KYC in the same way centralized lenders do. For many users, that’s the point. You connect a wallet, supply collateral, and borrow directly through smart contracts.

The flip side is user responsibility. Gas fees, wallet security, and liquidation management are on you. If you want fiat in your bank account, Aave isn’t built for that.

Pros:

- No KYC for standard onchain use

- Large liquidity and multi-chain access

- Transparent, non-custodial design

- Best DeFi lending platform

Cons:

- Variable rates can rise fast

- No simple fiat off-ramp

- Less beginner-friendly than CeFi platforms

- More responsibility is on you

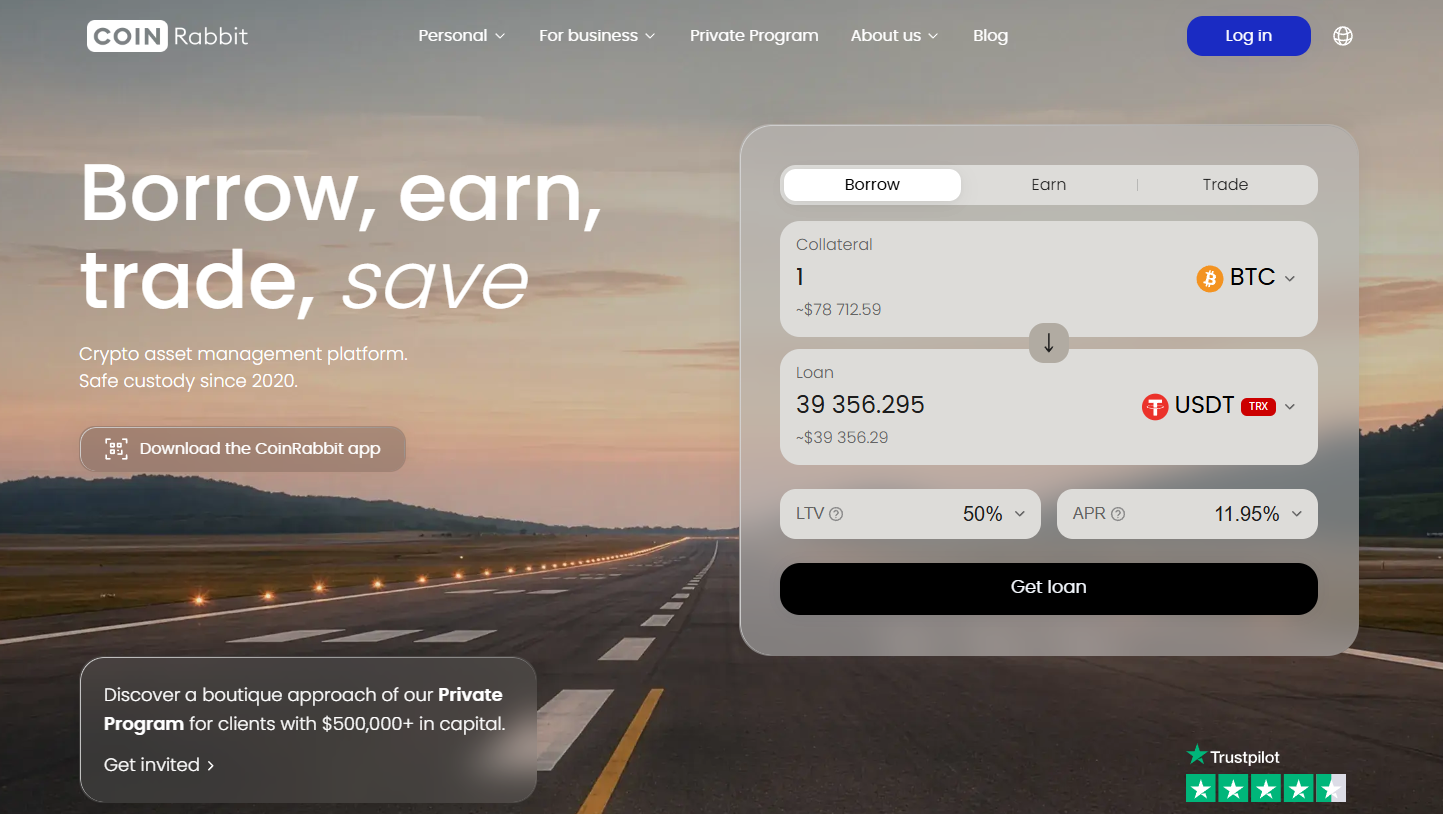

3. CoinRabbit

Best for: fast option with higher borrowing power

If you need speed more than polish, CoinRabbit is one of the more direct options in 2026. It has a very simple pitch: fast loan setup, no credit checks, and broad collateral support.

The platform offers flexible borrowing and relatively high LTV choices, with published ranges around 50% to 90% and APRs around 14% to 17%. That higher borrowing power can help if you want to free up more capital from the same collateral stack.

That’s also the risk. The closer you borrow to the edge, the less room you have when prices fall. High LTV can feel efficient right up until the market turns.

CoinRabbit is great if you want quick access, flexible collateral choices, and less paperwork. As mentioned in our in-depth CoinRabbit review, it doesn’t require KYC, which is relatively rare for centralized platforms.

However, it may not be a great fit for cautious borrowers who want wide safety margins.

Pros:

- Fast approval and simple process

- No credit checks, broad asset support

- Higher LTV options than many rivals

Cons:

- Higher borrowing risk at aggressive LTV levels

- Rates are on the expensive side

- Custodial model, with some regional restrictions

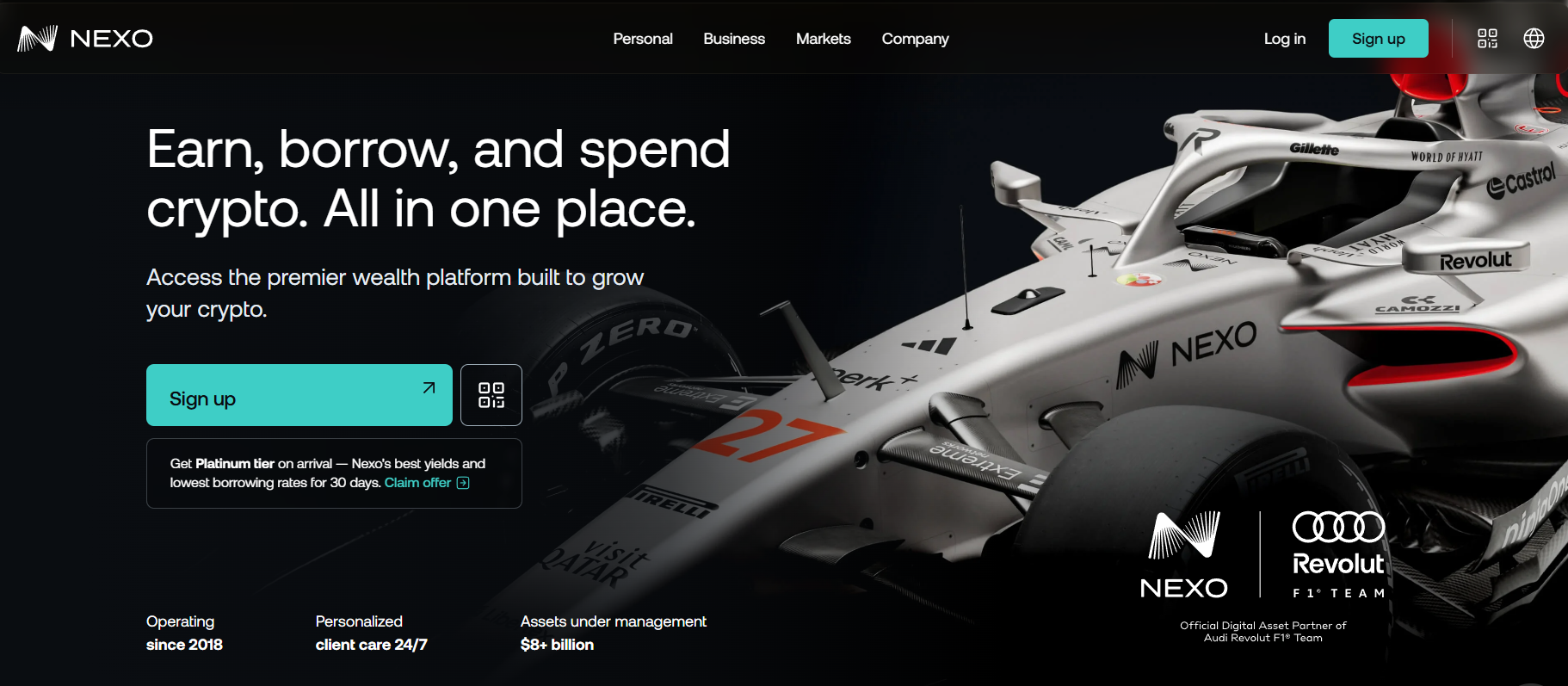

4. Nexo

Best for: flexible all-around platform for larger portfolios

Nexo is great if you want one account to do several jobs. Borrowing, spending, earning, and portfolio management all sit in the same system, which makes it attractive for larger or more active holders.

Its credit line model is a big part of that appeal. Instead of a strict fixed-term loan, you can draw against your collateral and pay interest on what you use. The platform supports 60+ cryptocurrencies, with borrowing available in fiat or stablecoins. Pricing varies by loyalty tier, and holding the native token can improve rates, sometimes sharply.

That setup is convenient, but it adds a layer of platform economics you need to understand. If you don’t want your loan pricing tied to a token-based loyalty system, Nexo may feel less clean than a simpler lender.

Still, for users with diversified holdings, Nexo is one of the easiest all-around choices.

Pros:

- Broad asset support and flexible credit lines

- User-friendly app and account tools

- Good fit for larger multi-asset portfolios

Cons:

- Best pricing may depend on holding NEXO tokens

- Terms can feel less straightforward than fixed loans

5. Nebeus

Best for: stablecoin and capital-efficient borrowing with fiat rewards

Nebeus has built a clear lane for itself. It’s a practical option for users who want different loan types, stable-asset flexibility, and easy access to fiat rails like EUR and GBP. It’s regulated by the bank of Spain.

The main reason it’s on my list is capital efficiency. Reported LTV limits go as high as 95% for stablecoin-based loans, while other asset types are more conservative, around 50%. That makes Nebeus interesting for borrowers who hold stable assets and want to unlock cash without posting large amounts of volatile collateral.

It also helps that the platform is geared toward real-world payouts. If you want funds that move into everyday spending channels, Nebeus is easier to work with than a pure onchain protocol. Plus, you can choose which currency to get rewards in, including both crypto and fiat currencies.

This is still a custodial service, so the usual platform risk applies. But for users who care about stablecoin borrowing or European fiat access, it’s a strong fit.

Pros:

- Multiple loan types for different strategies

- Strong option for stablecoin-backed borrowing

- Useful fiat payout features, including EUR and GBP access

- Regulated by the bank of Spain

Cons:

- Custodial platform risk

- Less appealing if you want pure DeFi control

- Rates vary by loan type, so comparison takes work

6. Binance Loans

Best for: the convenience of a major crypto exchange

Binance Loans makes the most sense if you’re already inside the Binance ecosystem. If you trade there, hold assets there, and want quick access to borrowing, the convenience is hard to beat.

As one of the best crypto exchanges, the platform supports a large range of assets, with 400+ cryptocurrencies as collateral across Binance products.

Borrowing terms and rates vary by asset and market conditions, but the key selling point isn’t novelty. It’s that using Binance is very fast and convenient. You can move from collateral to borrowed funds without leaving the exchange you’re already using.

That’s useful for active traders who care about execution and low friction. It’s less attractive if you want to spread risk away from exchanges.

So the biggest strength is convenience. The biggest weakness is concentration risk.

Pros:

- Easy for existing Binance users

- Broad asset support

- Convenience of a top-tier crypto exchange

- Good fit if you want both borrowing and trading within the same platform

Cons:

- You take on exchange risk

- Terms vary a lot by asset

The bottom line

The best crypto lending platform in 2026 depends on one thing first: your goal. Are you protecting Bitcoin, moving fast, borrowing onchain, or freeing up capital from a bigger portfolio?

You should pick a platform that matches your assets, your risk tolerance, and how much control you want. Safety, rates, and usability matter more than hype.

Compare loan terms, liquidation rules, and custody practices before you borrow or lend. That’s where the real differences show up.

FAQ

What are crypto lending risks?

The main crypto lending risks are:

- Liquidation

- Platform failure

- Smart contract bugs

- Changing interest rates

- Loss of collateral

If your collateral drops too much in value, the platform may sell part or all of it to protect the loan. There is also custody risk with centralized platforms. If the company freezes withdrawals, becomes insolvent, or changes terms, you may not have full control over your assets.

Is crypto lending safe?

Crypto lending can be safe enough for experienced users who understand the risks, but it always has risks. Even reputable platforms can expose you to liquidation risk, custody risk, or smart contract risk.

The safest approach is to use conservative loan-to-value levels, avoid borrowing too close to the liquidation point, and choose the right platforms.

Crypto lending vs staking: What’s the difference?

Crypto lending means you lend your crypto to earn interest, or borrow against your crypto by using it as collateral. Staking means you lock up proof-of-stake assets to help secure a blockchain network and earn rewards.

The main difference is where the yield comes from. Lending yield usually comes from borrowers paying interest, while staking rewards come from blockchain validation.

Is it a good idea to lend crypto?

It depends. Lending crypto can be a good idea if you want to earn passive yield and you understand the risks. It may make sense for long-term holders who do not want their assets sitting idle.

But lending is not the same as keeping crypto in a wallet. You may be giving up control, taking platform risk, or depending on smart contracts. If you care about safety more than earning yield, it’s better to avoid lending or only lend a small portion of your portfolio.

Are crypto backed loans legit?

Yes, crypto-backed loans are legit when offered by real platforms with clear terms, proper collateral rules, and transparent operations. They let users borrow fiat, stablecoins, or crypto without selling their holdings.

However, not every platform is equally trustworthy. Before using one, check the loan-to-value ratio, liquidation rules, fees, custody model, supported assets, and the platform’s track record.